Part 1 of this two-part series looks at the importance of leveraging social media contextually in the banking industry. The example of a credit card is used to illustrate how social media can be used at each stage of the generic buying process to establish a connect with customers, starting with the first stage: Need Recognition and Problem Awareness. The remaining four stages are addressed in this installment.

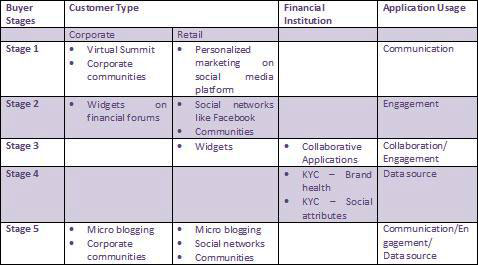

Stage 2: Information Search

The second stage deals with customers looking out for the right information in order to shortlist potential alternatives.

Corporate banking customers might look for references in the leading financial publications and case studies. A retail customer would be more interested in visiting bank websites and seeking word-of-mouth referrals.

Considering the references used by both, social media have applications that can be used to disseminate information to both parties. A public social network like Facebook provides an ideal platform to engage with retail customers. Also, dedicated retail bank communities can be used for word-of-mouth referrals.

For corporate, the best way might be to provide a widget on leading financial forums through which the company can give brief information about itself and invite requests for case studies and related material.

Stage 3: Evaluation of Alternatives

The third stage is decisive for both parties, as it's at this point that one organization is differentiated from the others. The alternatives have been filtered after the information search; hence both parties will likely use this stage to compare tangible factors more than anything else.

In the corporate scenario, this stage is mainly governed by the actual discussion of contractual terms and what best terms could be provided by the FIs. A physical meeting is more or less required at this stage; hence, social media will function less as a channel of external communication than as a channel of collaboration.

The FI representative can be given an application on a mobile device that will enable real-time assistance from the team back at the office to provide the best offers and answers to the customer.

In the retail scenario, this stage will be an extension of earlier activities. Now the focus of the customer will shift to getting specific answers about interest-free periods, annual fees, merchant tie-ups and so forth. An unbiased comparison is what customers are looking for; hence, the influence of the FI is very negligible.

Still, in order to ensure the customer is won, social media can be used by the organization as an engagement tool. Widgets can be of value, allowing customers to enter their preferred choices. Based on those results, personalized offers can be displayed.

Stage 4: Purchase

An organization may heave a sigh of relief if it is able to get a customer to this stage. However, this is where the actual work starts. The customer has a set of expectations derived from those points on which your organization made the best sell, but now it is the time to show that those expectations will not only be met but exceeded.

Customers are very receptive when starting a new relationship, and this is where social media should be leveraged to helping create a strong foundation for customer trust.

Both the parties will love the personalized attention. The FIs need to make their on- boarding a hassle free experience. The most time-consuming activity of the whole purchase cycle is the KYC (Know your customer) process. The sensitive nature of this exercise definitely rules out complete automation, but here too social media can be utilized for new data points.

For a corporate customer, brand health reports can be obtained using social analytics tools. The FI can get to know about the community perception and the employee perception by scanning various influential forums where the company is always talked about.

Similarly, in the case of retail customers, FIs can use a person's social profile on LinkedIn, Facebook and other sites to identify influences and other social characteristics.

Stage 5: Post-Purchase Evaluation

Customer service and retention activities are the prime focus at this stage. Once customers actually start using a product, service issues can be expected to varying degrees. Hence, it is vital for the organization to be easily accessible. Social media applications like Twitter can be used as official service channels.

By using social media as service channels, an organization can bring about real cost savings and also -- considering that most retail users are hooked on one of these channels -- shorten the adoption/learning curve.

The representation here speaks clearly about the scope of social media as an avenue. Going to this level, however, will require a clear strategy in terms of approach, design, execution and objectives.

This article has highlighted the practical use of social media applications throughout the buyer cycle for corporate and retail customers. The first step in this direction is to get familiar with social media and then connect the channel with CRM processes.

There may be challenges in seamlessly integrating the social media channel with the existing CRM system. However, given how the market is shaping up, CRM vendors and consulting provider/solution integrators will be ready to ease the way to social customer relationship management.

Nishith Gupta is an associate consultant with the enterprise solutions unit at Infosys Technologies, where he focuses on new go-to-market CRM solutions. Nishith blogs on Customer Retention, Social CRM and Campaign Management at theInfosys Blog on CRM.

Good Article!

This poses a real challenge in short form media (Tweets, Facebook status updates, or Foursquare check-ins). Here at CMP.LY we have been on the forefront of these issues. We have developed an emerging standard that makes compliance and disclosure straightforward.

CNN Money posted an article about CMP.LY and our solutions to transparency and accountablity yesterday:

http://money.cnn.com/2010/12/01/technology/paid_blogger_disclosure/index.htm?source=yahoo_quote

The guidelines may be complex, but the solutions can be simple.

and, of course, my disclosure:

http://www.cmp.ly/4/co2loq